The BUDGET

While I prefer not to focus on discretionary testamentary trusts generally in my content as there are so many out there doing a better job, it is hard not talk about them this week. Will the tax changes announced in the budget result in a new tax on discretionary testamentary trusts? While I have strong personal opinions on the likelihood of this, for now we don’t know.

However, let’s pretend that the tax does impact DTTs. What does that mean for you as an Estate Lawyer?

Why do we use Discretionary Testamentary Trusts?

It is easy for me to say, this doesn’t matter, because I have always been tax agnostic. I have always told my clients that tax will happen, make the decision that works for your family. However, that doesn’t really answer the question of what happens if there is a tax, and why do we use DTTs if they will be taxed at the new rate?

How about we look at all of the reasons that we use a Discretionary Testamentary Trust. Those reasons include -

control - you aren’t just choosing beneficiaries, you are choosing Trustees and Appointors who can both provide different but important protections moving forward

separate legal entity - this is about asset protection, it is also about not involving your in laws in decision making because the separate legal entity means that the financial decisions of the couple don’t impact the financial decisions of the trust (and vice versa)

straw man - you make it easier for all of your beneficiaries to say no, they can say “I would have to get everyone to agree” or “it isn’t mine, the trust owns it”

timing - the family doesn’t have to decide whether or not to sell assets, or transfer them into the name of the beneficiaries, they can put it into the testamentary trust and come back to it in two year’s time

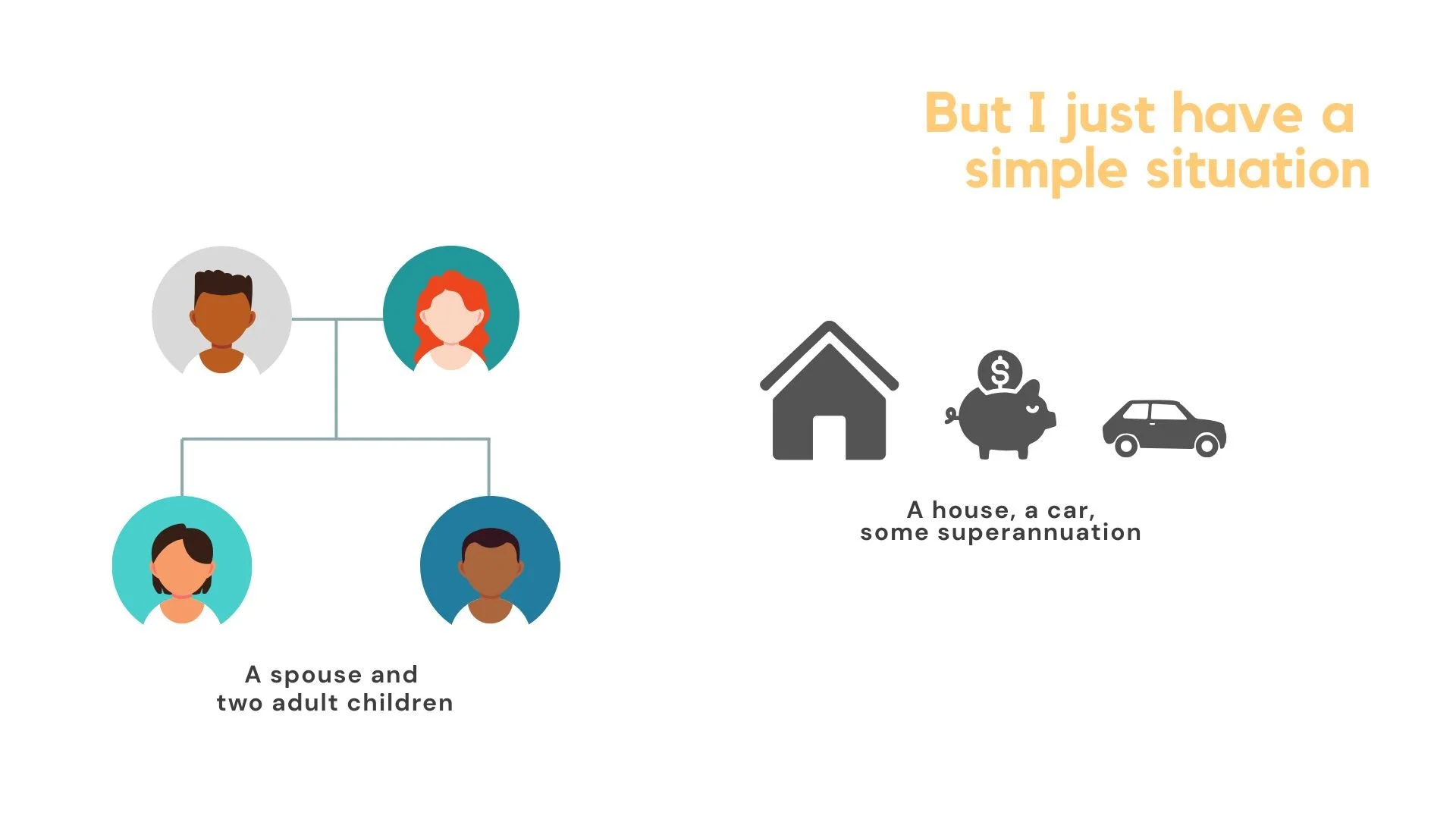

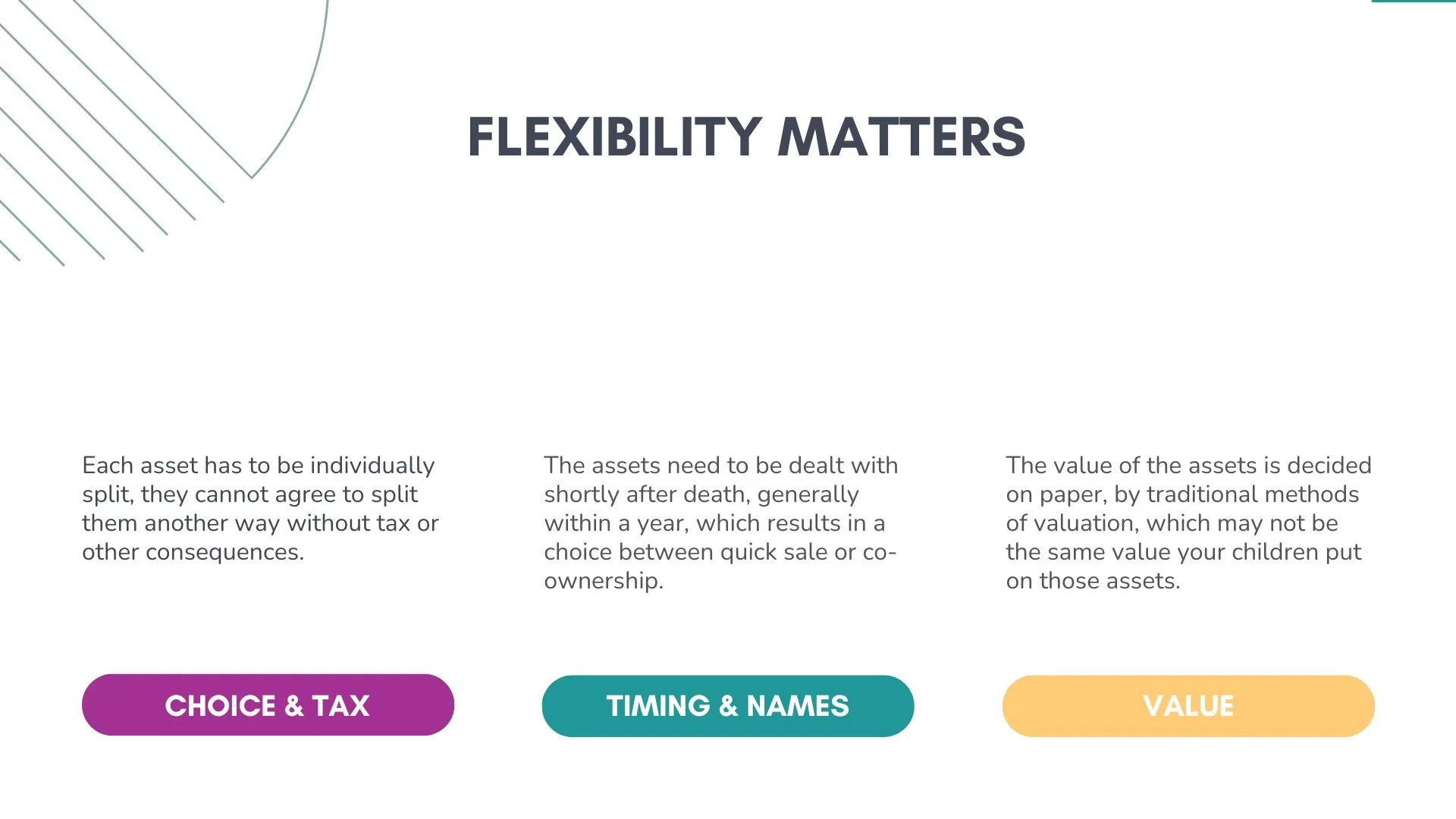

paper values - when apportioning assets under a simple “I love you” Will you are normally stuck with paper values of assets, even if the family agree that things have different values and that breaking it up in a certain way is, for whatever reason, equal and fair

individual assets - a basic Will requires a division of each and every asset, not a global approach to the total value of the Estate, and some assets in particular (like real estate) will attract fairly significant costs (like stamp duty) if they aren’t dealt with by splitting it “equally” amongst the beneficiaries

safety net - if you want inter-generational wealth, or a safety net that your child will still have when it comes time for them to retire, it is difficult to imagine this happening if the assets are simply cashed out and used to pay down debt

choice - a properly prepared Discretionary Testamentary Trust precedent should give your clients the choice between the DTT and a simple, direct inheritance, so they don’t have to guess now whether or not the tax will be advantageous at time of death

next generation - with a trust it is significantly easier to include the next generation, perhaps through a gift and loan back arrangement, in a way that helps give the grandchildren a leg up without fully exposing the inheritance to youthful indiscretions

family provision claims - if you decide to split your joint tenancies and put your spouse’s inheritance into the trust, it means that the asset isn’t available to your spouse’s Estate (bearing in mind some specific decisions will be needed to avoid notional estate in NSW)

include the aunt or god mum - one of the things I talk to most clients about is the ability to include the trusted Aunt or God Mum as an appointor with the children, so that they can step in if there is someone in the life of one of your children who is exercising undue pressure, but if everything is going well they can retain their sideline position

market conditions - imagine if your loved one had just died, and then some budget announcement was made that potentially reduced the value of an asset that you now need to sell. Crazy right? Do you want to be left with a choice between selling it cheaply, or co-owning an asset with your sibling, in your personal names?

There are other possible advantages, like separating the Appointor and Trustee positions so that your adult child can be the Trustee at 25 years old but cannot be the Appointor until 35 years old. On the whole though the point is that the Discretionary Testamentary Trust allows for the flexibility to make decisions that are relevant at the time of your death rather than guessing what is needed now.

Explaining it to the clients

Again while I don’t consider myself an expert on Discretionary Testamentary Trusts, but I did cover some of these reasons in my recent Webinar which was focused on the “I just want a simple Will” problem that we face as solicitors. In that Webinar I went through how I would explain to a client that they don’t want a “simple Will” and as it so happens, many of those reasons are completely tax free.

If you would like to get the slides, and the recording of the Webinar, then click on the button below. It costs $90 to get the recording and the precedents.

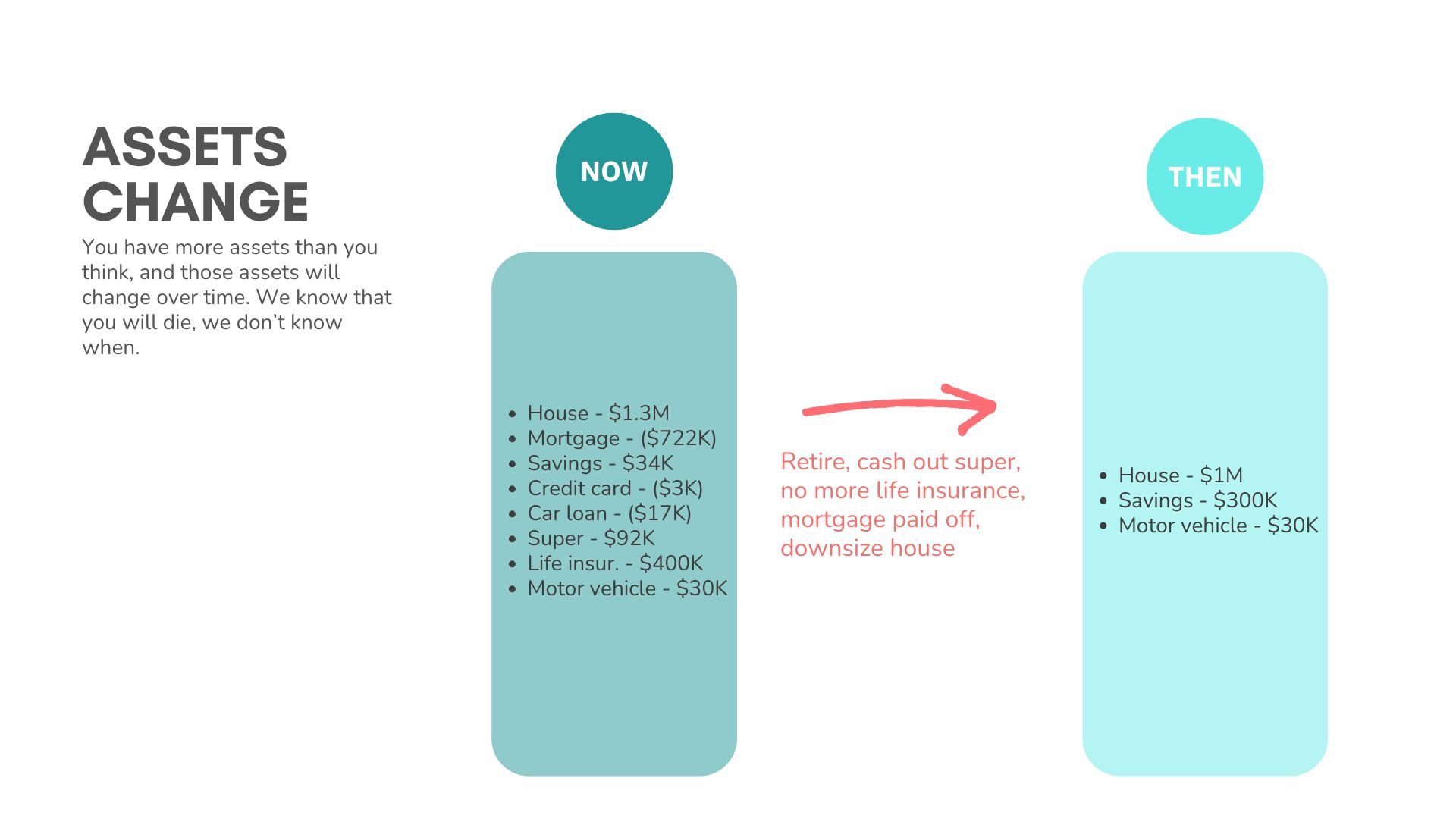

Assets change

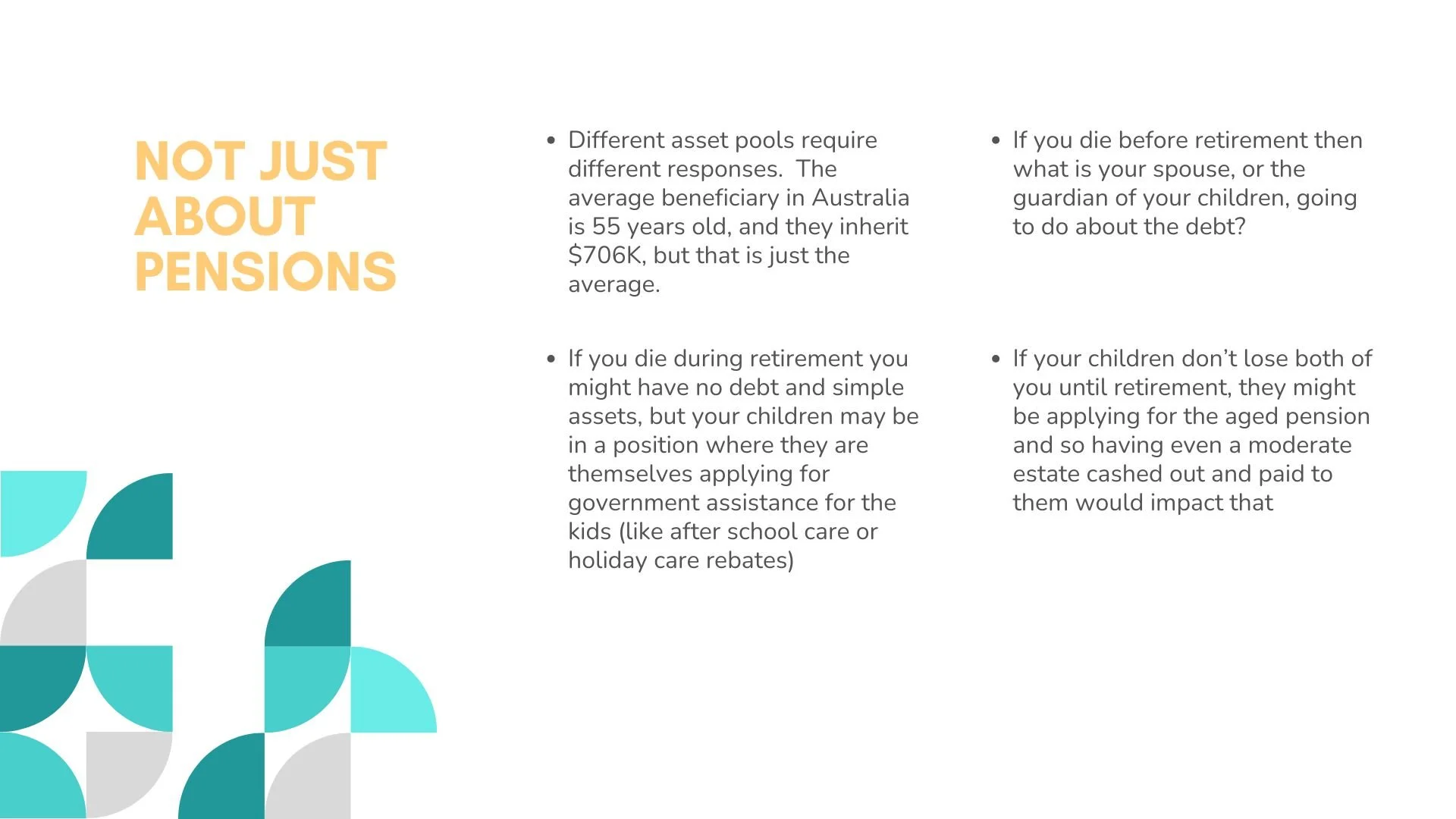

One of the problems with preparing an Estate Plan is that your assets now may be very different to the assets that you have at retirement. Can you prepare an Estate plan that deals with both of those situations? If you die now, what is happening with all of the debts? If you die during retirement, will your spouse inheriting all of this suddenly impact their access to the pension?

Government pensions or allowances aren’t actually just about the old aged pension or the disability pension. They aren’t just about the cash payment. It is also about continued access to programs, either social programs or medical programs that are only available to pensioners. What if your spouse had to move, or stop attending a weekly event, because they lost access to the pension?

It is also about your adult children still qualifying for the subsidised after school care or vacation care, and if you and your spouse live long enough it may be your adult children applying for the aged pension shortly after your death.

Now because the Webinar wasn’t specifically about DTTs, it was about clients who “just want a simple Will” some of the issues raised can be solved by a comprehensive Will which includes things like apportionment clauses, but the points made still provide relevant information for this more recent issue of, what if a DTT doesn’t have tax advantages anymore?

If you want more information about that Webinar than click on the button below.